An internal audit commissioned by Augusta Mayor Hardie Davis shows that the Mayor’s Office violated both state law and city procurement procedures with the use of a city-issued credit card.

While making recommendations on how to comply with the law going forward, the audit does not address how to handle previous violations of the state code.

The mayor’s self-imposed audit was provided to Richmond County Commissioners this past Friday, July 30. The report is referred to in the document as an internal audit, and it uses the word “audit” throughout. However, the author of the report is very clear that accounting firm Serotta Maddocks Evans & Co., did not perform an actual audit. Instead, the firm performed consulting services.

The first sentence of the document states, “We have performed consulting services.”

READ THE ENTIRE AUDIT REPORT HERE

Mayors Office Self Audit by augustapress on Scribd

A few paragraphs later, the report clearly states, “We were not engaged to, and did not conduct an audit, the objective of which would be the expression of an opinion on the financial statement, or an element of a financial statement.”

This leaves the door open to protect the accounting company. The reports introduction states, “Had we performed additional procedures, other matters might have come to our attention that would have been reported to you.”

MORE: Mayor Fails To Produce Resume Purchased Using Taxpayer Funds

MORE: Mayor Preemptively Calls For Audit

As noted in the section of the report titled “Credit Card,” the city has not “promulgated specific policies,” as required by GA Code § 36-80-24 (2015). Therefore, the use of the mayor’s credit card by his office has not always been in compliance with the Georgia code, according to the report.

In reference to elected officials’ use of a credit card, Georgia Code § 36-80-24 states, “Such purchases [must be] solely for items or services that directly relate to such official’s or constitutional officer’s public duties; and Such purchases are in accordance with guidelines adopted by the county, municipal corporation, local school system, consolidated government, or constitutional officer.”

Further, the code requires that “Documents related to such purchases incurred by such elected officials or constitutional officers shall be available for public inspection.”

Davis has failed to provide dozens of invoices or receipts for charges for 2020 and 2021 even when requested under the Georgia Open Records Act.

Additionally, under the code, no credit card is to be issued to an elected official after Jan. 1, 2016, unless appropriate policies are in place and a public vote by the city, county commission or other local government entity has occurred. Neither of those have occurred in Richmond County.

In addition to violating the state code, the audit notes violations of the city procurement policy. For example, Davis’s chief of staff, Petula Burks hired LC Studios, LLC, a firm that she had a previous relationship with while working for the city of Miami Gardens, Fla. The LC Studios owner is listed as an office of a Florida non-profit that Burks controls. Mayor Davis has denied any conflict of interest with the use of the Florida firm and its owner relationship with Burks.

The Mayor’s Office paid LC Studios, LLC, $24,969 between December 2020 and March 2021, according to the auditor’s notes.

“This amount exceeds the $10,000 threshold described in the city’s procurement policy” the report states. “The City’s procurement policy also includes a preference for local vendors.”

City procurement policy can be found HERE. The threshold for transactions to have to go through the procurement department is $5,000, not the $10,000 that the audit references.

The $5,500 payment to Burks a week before she was hired by the mayor was not addressed anywhere in the audit, even though that payment also violates the procurement policy.

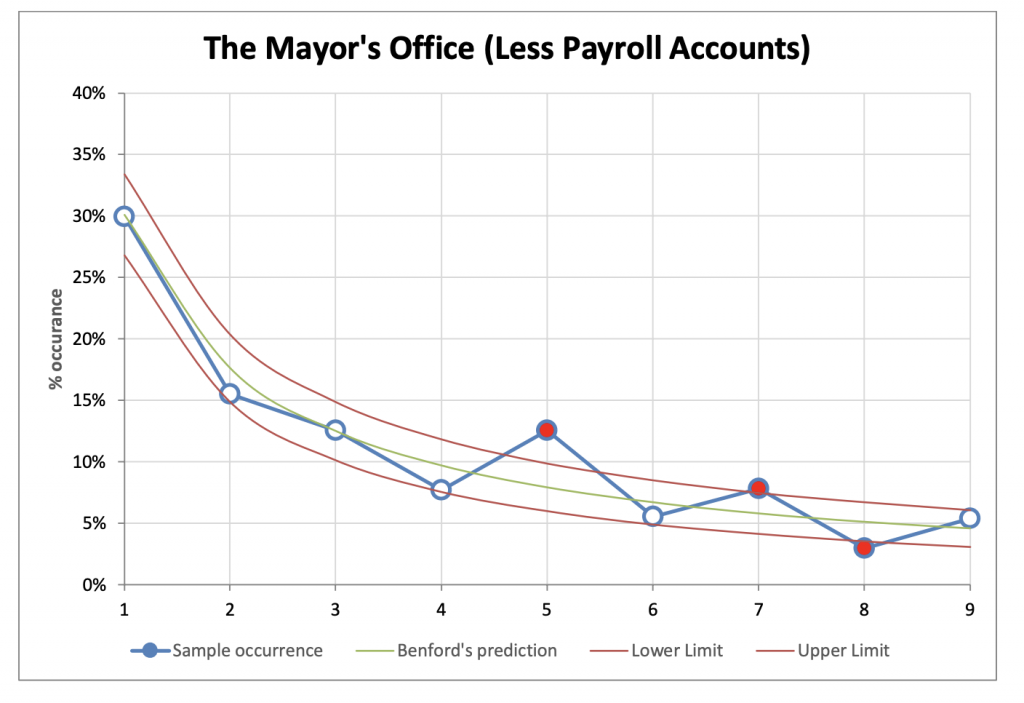

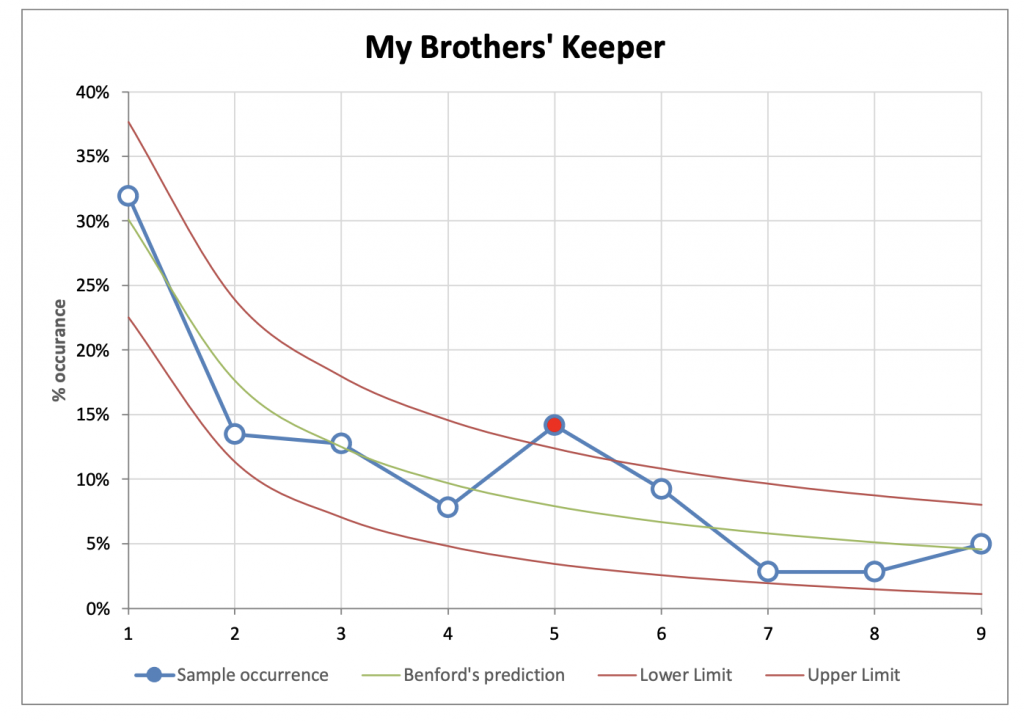

The accounting firm used an analytical method called Benford’s Law to examine the mayor’s credit card use. This is an accounting process that assists auditors in finding fraud, according to the report. Use of Benford’s Law revealed several irregularities that led the auditor to further scrutinize several transactions.

Both the mayor’s operating account and his My Brothers Keeper account had specific transactions that received additional scrutiny that are not outlined but that led to the recommendation to adopt a credit card policy, follow city procurement guidelines and provide copies of invoices or receipts for all transactions.

The Benford Analysis might not have been the best methodology to use to scrutinize the Mayor’s Office’s spending. According to an April 2017 article by Certified Public Accountant L. Carlton Collins, writing in the Journal of Accountancy, “Benford’s Law works better with larger sets of data.

MORE: Augusta Commission Makes First Step in Reining in Mayor’s Credit Card

MORE: Scrutiny And Stonewalling Continue Over Augusta Mayor’s Spending

“While the law has been shown to hold true for data sets containing as few as 50 to 100 numbers, some experts believe data sets of 500 or more numbers are better suited for this type of analysis,” according to Collins.

Fewer than 50 transactions were used in the Benford Analysis of both the mayor’s operating and the separate account for My Brothers Keeper.

Collins goes on to explain that the analysis cannot definitively prove or disprove fraud.

“If the chart doesn’t closely follow Benford’s curve, then consideration should be given to scrutinizing the data more carefully,” Collins sated.

Both of the mayor’s accounts showed an irregular curve on the Benford Analysis indicating that additional analysis was required of multiple transactions.

Commissioner John Clarke and several other commissioners believe a forensic audit is needed. Clarke’s motion for a forensic audit of the city’s accounts failed to move forward.

According to a 2020 article by Doug Cash, a certified fraud examiner with Eide Bailly, noted as one of the top 25 CPA firms nationwide, audits are to be done by auditors that are independent.

MORE: Mayor’s Office Credit Card Audit Fails in Commission

MORE: Augusta Mayor’s Financial Records Produce More Questions Than Answers

The report provided to Richmond County Commissioners was not independent because the party being audited engaged the CPA firm.

Financial audits differ largely from forensic audits in that they evaluate income and expense as well as whether a company is losing money, according to the article.

Forensic audits are “an examination of financial records to find any illegal financial activity,” according to Cash’s article.

“A forensic audit employs different types of investigative techniques than those used in a financial audit and gathers evidence for use in a civil or criminal court of law,” according to Cash.

According to Cash, a forensic audit would be used to determine if someone was misappropriating money according to the report.

Serotta Maddocks Evans & Co. had a very narrow scope of investigation for their analysis. The report failed to mention multiple inconsistencies that have been reported by Augusta media in recent months.

Items not addressed in the report include the following:

- P-Cards. The Mayor’s Office P-card stopped being used in March 2020 with the departure of staffer Marcus Campbell. The credit card was used going forward, and the more regulated P-card has not been used by Davis since. Several vendors who were paid with the more regulated P-card in 2019 and early 2020 were paid with Davis’s credit card in 2020. This included payments to The Message Moguls, a company owned by Lynthia Ross the current information officer for the Richmond County Board of Education.

- PayPal. No mention of whether PayPal charges violate city policy or if vendors should be paid through that online method. Petula Burks was paid $5,500, and multiple payments to The Message Moguls occurred in 2020. Open records requests indicated that none of those transactions were reported by the city to the Internal Revenue Service.

- 1099s. Multiple questions have been raised as to whether paying vendors with credit cards or PayPal violate IRS standards for reporting income. Vendors paid with a Augusta credit card are not having the income reported to the IRS.

- Davis’s increased spending from an average of $2,500 per month in previous years to over $10,000 per month on average the first few months of 2021.

The report recommends that the mayor provide invoices or receipts for all charges. The auditor also recommended that Davis follow city procurement policies and in particular be make note of the policy when hiring an out-of-town vendor. In addition, it was recommended that the city adopt a credit card policy, which is something that was already approved in recent weeks by the county commission.

Joe Edge is the Publisher for The Augusta Press. Reach him at joe.edge@theaugustapress.com.

{kind=link}

{kind=link}

{kind=link}